Examining the Gap: Why Isn’t Personal Finance Taught in School?

Last reviewed: June 2026

Why isn’t personal finance taught in school, despite its undeniable importance in adulthood? It originates from deep-rooted educational customs, an excessive focus on standardized testing, and a limited perspective that presents a singular trajectory in life, which involves a lack of understanding of financial principles.

This article investigates the reasons behind excluding personal finance from school curriculums and discusses the effects of this educational void.

Key Takeaways

Historically, the education system has neglected financial literacy, focusing on standard academic subjects and test scores while lacking real-world financial education, contributing to a deficiency in Americans’ financial knowledge.

Teachers often lack the proper training and resources to effectively teach personal finance, posing a challenge to integrating these essential life skills into the school curriculum.

The push to incorporate personal finance into educational programs is vital, given the clear advantages of making informed financial choices for lifelong prosperity. This highlights the critical importance of advocating for changes in educational policies at the state level.

Unpacking the Education System: Why Isn’t Personal Finance Taught in School?

Historically, the education system’s focus has been on academic subjects, with financial literacy being a neglected topic on the educational agenda.

In fact, financial literacy is not a prioritized subject in the traditional school curriculum. This lack of focus on financial education contributes to a deficiency in financial knowledge among Americans.

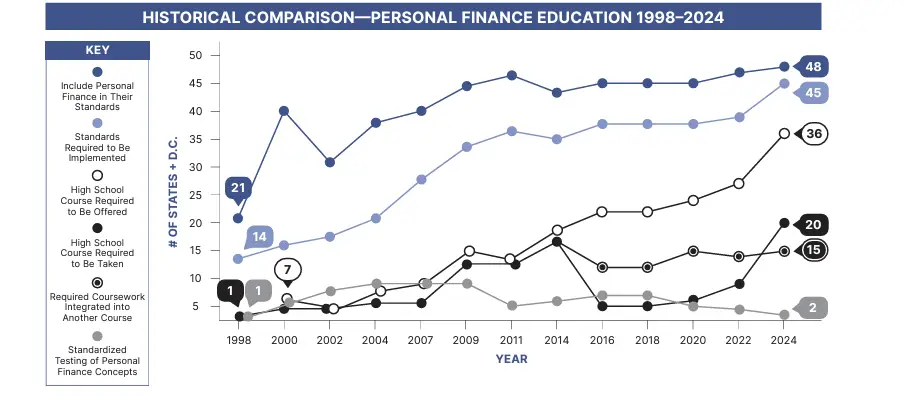

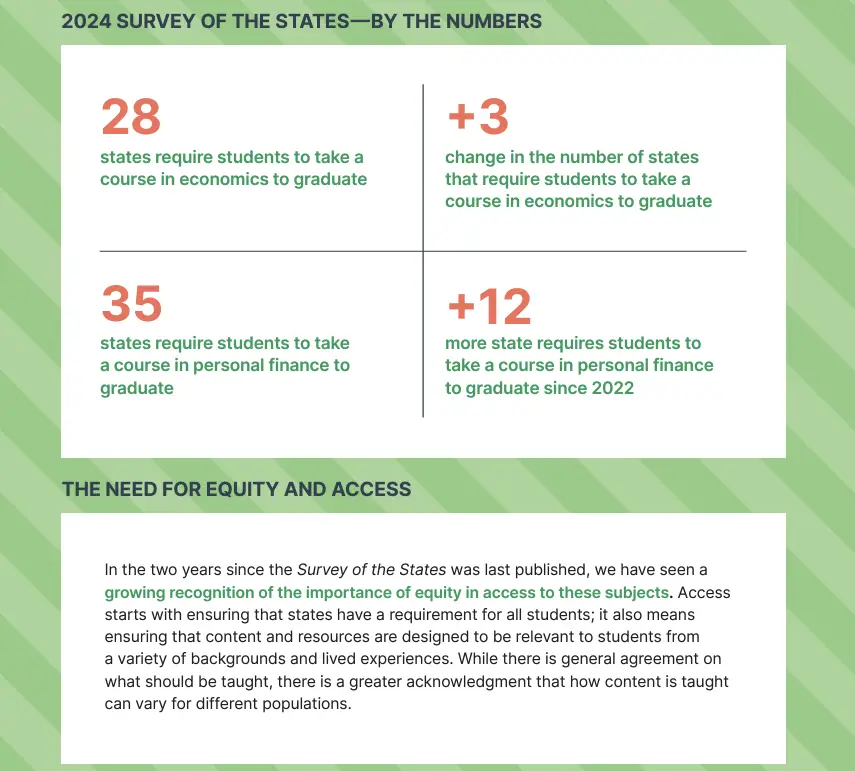

The numbers back up the claim – The statistics support the assertion – Currently, 22.7% of high school students in the United States are assured a personal finance education.

This means that nearly 1 in 4 of the graduating class of 2022 will have been equipped with the necessary knowledge to handle their finances with competence!

So, why has the education system traditionally prioritized certain subjects over personal finance? The answer lies in the legacy curriculum and the prioritization of standardized testing over life skills.

The Legacy Curriculum

Historically, personal finance has not been considered a core subject and was not taught in school. Instead, traditional educational approaches insisted on uniformity and mastering step-by-step arithmetic algorithms, with little emphasis on practical applications or life skills like financial literacy. The focus was mainly on ensuring that all students were on the same page, rather than preparing them for real-life financial situations.

This approach to teaching has, unfortunately, left a void in the education system. Many students graduate without the necessary skills to manage their personal finances, leaving them vulnerable to financial pitfalls in adulthood.

Prioritizing Standardized Testing Over Life Skills

If you’ve ever taken a standardized test like the ACT or SAT, you might remember that personal finance was excluded from the test.

That’s because standardized testing typically focuses on academic subjects that can be easily measured across different locations and schools, neglecting practical life skills such as financial literacy.

In other words, the education system has prioritized test scores and academic achievement over practical life skills.

The teaching strategies used for subjects that are part of standardized tests, such as memorization and repetition, do not align well with the teaching of personal finance, which benefits from a practical, hands-on learning experience.

This systemic prioritization has inadvertently created a generation of students who excel in academics but lack the necessary skills to manage their personal finances.

Bridging the Knowledge Gap: The Role of Teachers and Resources

While the education system plays a significant role in the lack of personal finance education, the importance of educators and available materials cannot be understated in this equation.

Some of the challenges include:

Teachers often lack the specialized training necessary for effective financial education

There is a lack of dedicated financial education teaching materials

Insufficient guidance on the usage of available resources

Addressing these challenges is essential to improving financial education in schools.

Furthermore, integrating real-world financial issues into the curriculum in an engaging manner poses a challenge for teachers.

Even those who are enthusiastic about improving financial literacy might not feel confident in their own financial knowledge to teach the subject.

Let’s take a closer look at the influence of educators and available materials in the realm of personal finance education.

Teacher Preparedness for Financial Topics

Teaching personal finance isn’t as simple as teaching arithmetic or history. It requires a unique set of skills and knowledge.

For effective personal finance instruction, teachers need to be equipped with both an understanding of financial concepts and the skills to convey these topics in a way that resonates with diverse student backgrounds.

However, many teachers often do not feel qualified to teach personal finance and face several challenges, with 63% citing lack of time and 13% citing lack of expertise as primary barriers.

To bridge this gap, programs like the Cowin Financial Literacy Program and Jump$tart Financial Foundations for Educators are designed to enhance teachers’ financial knowledge and instructional capabilities. These programs underscore the importance of a comprehensive strategy that includes:

Teacher training

Sustainable funding

Evaluations

A scalable program plan for effective implementation of financial education.

Availability of Quality Teaching Tools

Even with trained teachers, quality teaching tools are essential for effective financial education. Unfortunately, there is a shortage of comprehensive financial literacy teaching tools, with only a few websites offering mini-lessons, games, or interactives for students.

However, all hope is not lost. Educators have access to classroom-ready materials like:

case studies

political cartoons

videos

online platforms

These materials can be used to teach financial literacy, as provided by initiatives like the Cowin Financial Literacy Program.

Moreover, community-based initiatives, such as government-sponsored programs, can provide educational funding to support learning opportunities for students.

The Disconnect Between School and The Working World

The public school system, as a part of the education system, has traditionally valued academic knowledge for material advancement, often overlooking the development of skills necessary for navigating the modern professional landscape.

Older educational practices rely predominantly on teacher-centered methodologies, with an emphasis on:

memorization

regurgitation of information

standardized testing

passive learning

These practices prioritize the acquisition of knowledge over the application of knowledge in practical settings.

This approach has resulted in a critical disparity with the real-life financial skills required in today’s working world, as the typical school curriculum does not include financial education.

So, how can we bridge this disconnect and prepare students for real-life financial decisions?

Preparing Students for Real-Life Financial Decisions

Preparing students for real-life financial decisions is a critical aspect of education that is often overlooked. Practical financial skills are necessary for young adults to manage real-life challenges, but these are often not emphasized in schools.

Financial literacy education in schools can help students understand and connect with the real world, making education more engaging and relevant.

Exposure to basic financial literacy concepts in school equips young people with a foundational understanding of financial principles like:

compounding

budgeting

spending

saving

Core Skills Needed Beyond the Classroom

In addition to financial knowledge, skills like problem-solving, critical thinking, communication, teamwork, and innovation are critical for students to thrive in post-academic scenarios.

However, core financial skills such as not spending more than one earns, investing wisely, and being prepared for emergencies are seldom taught in schools, despite being essential for navigating life successfully after education.

This lack of core skills leaves many young adults ill-prepared for the financial challenges of the working world.

It begs the question, how can we ensure that the next generation is equipped with the necessary skills for financial success?

Parents’ Responsibility: Teaching Kids

While the education system plays a significant role in teaching personal finance, parents also have a crucial part to play.

However, most parents and teachers themselves lack personal financial management skills, highlighting the critical need to prepare the next generation to make informed real-life financial decisions.

So, what can parents do to improve their children’s financial literacy? Let’s explore how parents can encourage money talk at home and provide access to external financial resources.

Encouraging Money Talk at Home

Parents can play an instrumental role in teaching their children about personal finance and money management by modeling healthy financial habits, such as budgeting before shopping and saving for specific goals.

By incorporating children into everyday financial decisions and discussions, a transparent atmosphere around money matters can be fostered at home.

When children are included in conversations about finances, they learn to distinguish between shared family responsibilities and tasks that could potentially earn them money, thereby understanding the value of work.

Providing Access to External Financial Resources

In addition to modeling good financial habits and including children in financial discussions, parents can also utilize external financial resources to educate their children about personal finance.

The Consumer Financial Protection Bureau provides ‘Money as You Grow’ resources for financial education of children, including activities and conversation starters.

Moreover, there are several resources available to help teach personal finance to a wider audience:

Khan Academy offers free, accessible online courses on personal finance.

Children’s books tailored to different grade levels can serve as valuable tools for teaching various money concepts, as recommended by the Council for Economic Education.

These resources can be used to educate people of all ages about personal finance, including how to spend money wisely.

Taught in School: Personal Finance into Schools

Integrating personal finance education into schools can have a profound impact on students’ financial literacy. It can lead to:

more informed financial decision-making

reducing economic barriers

Improved financial education for economic empowerment

arming students with the necessary skills for sound financial decision-making and personal finance management

But what are the tangible benefits of this integration? Let’s explore how personal finance education can reduce financial mistakes among young people and build a strong foundation for future success.

Reducing Financial Mistakes Among Young People

Educational programs in personal finance can help young individuals avoid common financial errors, like excessive credit card debt or poor saving habits.

Teaching the basics of personal finance in schools creates foundational knowledge that can prevent students from making financial errors with long-term negative impacts.

Financial literacy allows individuals to handle a variety of financial instruments responsibly and reduces the likelihood of them making uninformed decisions.

Moreover, early education about personal finance helps people recognize financial literacy, reducing the severity and frequency of financial mistakes by allowing students to learn in a low-stakes environment.

Personal finance education also equips individuals with the knowledge to recognize and avoid financial scams and fraud.

Building a Strong Foundation for Future Success

Teaching financial literacy at a young age lays the groundwork for long-term financial health. Early financial literacy can lead to tangible benefits such as higher savings rates, improved credit scores, and a more stable economic future.

Individuals who receive financial education early are better equipped to achieve long-term financial goals, like saving for retirement or buying a home.

In essence, early financial literacy education not only reduces financial mistakes but also builds a strong foundation for future success.

Advocacy and Change: Pushing for Curriculum Reform

Championing personal finance education in schools requires more than just recognizing its importance. It requires action.

Gathering support from parents and guardians can significantly influence school administrators to consider integrating financial education into the curriculum.

Marketing personal finance as an elective and showcasing its value through student testimonies can increase enrollment and highlight the course’s impact.

Data showing the positive impact of financial education on students can be persuasive in spurring policy change at the school and district levels.

Networking and learning from other districts or states that have implemented financial education can help individuals become better advocates.

Advocating for financial education as a high school graduation requirement can set a quality standard and ensure its consistent implementation across schools.

Leveraging Community Support

To advocate for personal finance education, you can take the following approach:

Present the high level of student interest in personal finance education.

Back your argument with research on the benefits of financial capability in young adults.

Engage community members through participatory decision-making processes.

Implement effective educational changes.

This approach will help you make a compelling case for personal finance education, especially when considering a personal finance class to teach financial literacy.

Networking with educators and stakeholders in districts where financial education has been implemented can uncover effective strategies and provide a guide for successful community mobilization.

Creating a focused marketing strategy for money management classes that includes student testimonials can enhance awareness and boost enrollment, demonstrating the course’s value to the community.

Influencing Policy at the State Level

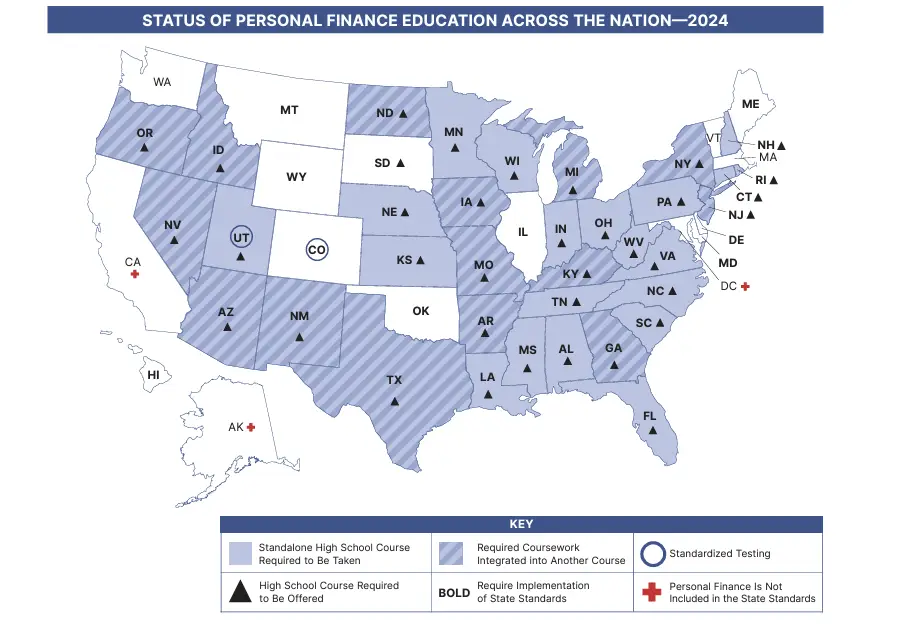

In the United States, educational content is determined at the state level, leading to inconsistencies in the inclusion of finance education.

This highlights the need for policy change at the state level to ensure consistent implementation of personal finance education across all schools.

By networking with educators and stakeholders in districts where financial education has been implemented, advocates can uncover effective strategies for influencing policy at the state level.

This can lead to the development of state-wide policies that prioritize personal finance education for all students, ensuring that every child has the opportunity to learn this essential life skill.

Summary

To sum it up, integrating personal finance education into schools is a complex issue with multiple stakeholders involved.

It requires a shift in the education system’s historical focus, the preparedness and resources of teachers, and the active involvement of parents.

The benefits of such a shift are immense, from reducing financial mistakes among young people to building a strong foundation for future success.

Advocacy and change are key in pushing for this curriculum reform. Let’s join hands in ensuring that our next generation is well-equipped to navigate their financial futures.

Frequently Asked Questions

Why financial literacy should not be taught in schools?

Financial literacy should be taught in schools as it is important for students’ future success and financial well-being.

It can help students make informed decisions and navigate complex financial systems effectively.

Why doesnt school teach about life skills?

Schools may not teach life skills because teachers may lack guidance and training, and may not feel confident enough to teach subjects like tax and personal finance.

It’s important to address this gap in education.

Why is financial education no longer part of the curriculum?

Financial education is no longer part of the curriculum due to the lack of federal mandates or guidelines, leaving educational decisions to be made on a state level.

This results in a lack of consistency in teaching personal finance.

What role do teachers play in financial education?

Teachers play a crucial role in imparting financial education, but they often lack specialized training and resources for effective teaching in this area.

What skills do students need for real-life financial decisions?

Students need practical financial skills such as budgeting, saving, spending, and understanding the principles of compounding, along with other core skills like critical thinking and problem-solving to make informed real-life financial decisions.

How many states currently require financial literacy education?

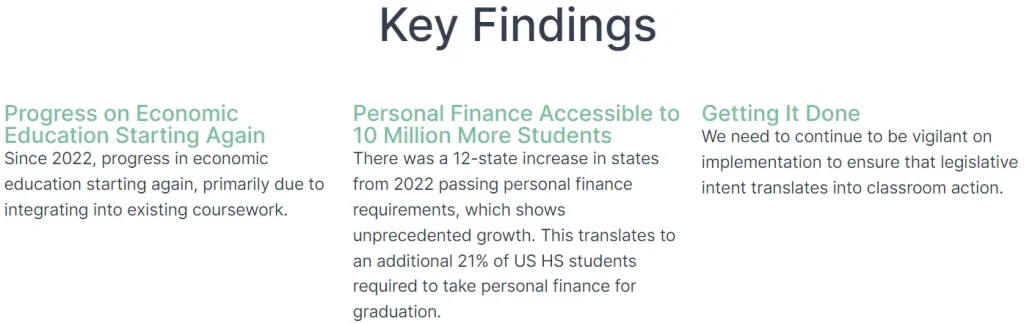

As of October 2025, 30 states require high school students to complete a standalone personal finance course for graduation. This represents significant growth from just 6 states in 2019, with states like Texas, Colorado, Kentucky, and Delaware recently passing requirements. Once fully implemented by 2031, approximately 73% of U.S. high school students will receive financial literacy education before graduation.

When do these state requirements take effect?

Implementation timelines vary by state, with most requirements being phased in over several years. For example, Ohio’s requirement started with the class of 2026, while Florida, Louisiana, New Hampshire, and Oregon requirements begin with the class of 2027. California’s requirement will be fully implemented for the class of 2030-2031, and several other states have similar phased rollouts through 2031.

Does financial education actually improve student outcomes?

Research shows that financial education has measurable positive effects on both knowledge and behavior. Studies indicate that students who receive financial education have higher credit scores, lower loan delinquency rates, and better savings habits compared to those without such education. The effects are particularly significant when programs include hands-on activities, are age-appropriate, and provide at least one full semester of instruction.

What topics are typically covered in high school personal finance courses?

High school personal finance courses typically cover essential money management topics including budgeting, saving strategies, understanding credit and debt, taxes, investing basics, and preparing for major financial decisions. Many programs also address topics like avoiding financial scams, understanding interest and compound growth, emergency preparedness, and planning for college expenses or career financial decisions.