What Is Term Life Insurance Mean: A Comprehensive Guide

Last reviewed: June 2026

Table of Contents:

- What is Term Life Insurance Mean? A Comprehensive Guide

- What Is Term Life Insurance?

- How Does Term Life Insurance Work?

- Key Features of Term Life Insurance

- Different Types of Term Life Insurance Policies

- Is Term Life Insurance Right for You?

- Before Getting a Term Life Insurance Quote

- The Cost of Term Life Insurance

- FAQs about what is term life insurance mean

- Which is better, term life or whole life insurance?

- How does term life insurance work?

- What happens to my term policy at the end of the term?

- Do you get your money back at the end of term life insurance?

- Can I renew my term life insurance after it expires?

- Can I cancel term life insurance early without penalty?

- Is term life insurance better than whole life insurance?

- What happens if I miss a premium payment on my term life insurance?

- Can I have both term and whole life insurance at the same time?

- Conclusion

What is Term Life Insurance Mean? A Comprehensive Guide

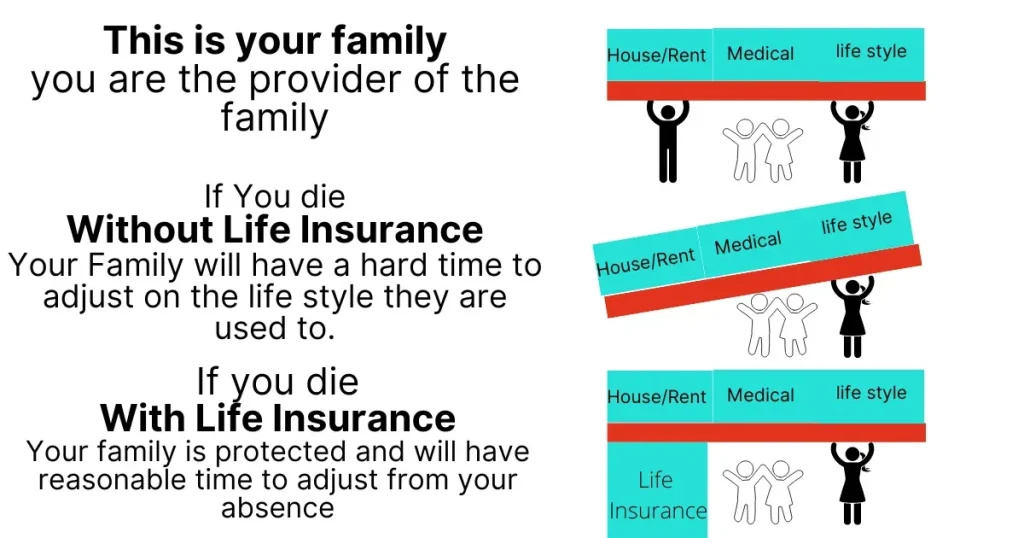

In today’s world, taking care of your family’s financial future is a big deal. This means thinking about what would happen if you were suddenly gone. That’s where understanding “what is term life insurance means” becomes really important. This type of life insurance acts like a safety net, offering protection for a specific period or term. So, if something unexpected happens to you during that time, your family will receive a payment that helps them cover things like mortgages, bills, and education expenses.

But with all the insurance companies and life insurance options out there, knowing how term life insurance works and if it fits your needs can be confusing. Let’s break down the basics.

What Is Term Life Insurance?

This life insurance covers you for a chosen number of years. This could be 10, 20, or even 30 years, giving you peace of mind that your loved ones will be financially supported if you die within this term period. The insurance term is the period the term life insurance policy is active.

How Does Term Life Insurance Work?

Imagine it like renting an apartment. You pay a regular amount, called a premium payment, and for as long as you pay rent, you’re protected. With term life insurance, you pay your insurance premiums regularly, and if you pass away during the term, the insurance company pays a fixed amount, known as the death benefit, to your chosen beneficiaries.

This money helps them pay off debts, handle living expenses, and continue living comfortably. Term insurance focuses purely on providing financial support if you pass away during the agreed-upon time. There’s no cash value buildup or investment element like with permanent life insurance policies.

However, many find that term life provides the most coverage for a more affordable premium cost. When you buy term life you are getting a guaranteed death benefit. This guaranteed death benefit is paid to your beneficiaries upon your passing.

Key Features of Term Life Insurance

- Affordability: Because term life provides coverage only for a set period, it generally costs less than permanent options, especially for young and healthy individuals. So “what is term life insurance mean” in terms of cost? You get significant insurance coverage without breaking the bank.

- Flexibility: Term life insurance lets you choose the coverage amount and term length. This means tailoring your policy to fit your personal finance needs and financial situation. As those needs change – say, your children grow up or your mortgage is paid off – you can adjust your coverage.

- Simplicity: Term policies are pretty straightforward to understand. You pay premiums for a certain period, and if you pass away within that timeframe, your loved ones get a payout. No investment components to worry about, no complex financial mechanisms to wrap your head around.

Different Types of Term Life Insurance Policies

From the outside, term life insurance appears simplistic, but as you get closer, you’ll realize it’s not quite that black-and-white, with various adaptations that can significantly impact your coverage. Life insurance options are plenty, with each term policy coming with its set of advantages and disadvantages.

Level Term Life Insurance

This is the most common form. It offers a fixed premium and death benefit for the entire policy term, keeping things nice and predictable for your budget. It’s one of the more popular types of term life insurance.

Increasing Term Life Insurance

Here, the death benefit rises over time. This is particularly useful if you anticipate your financial obligations growing (like a growing family) or if you want your life insurance to keep pace with inflation.

Decreasing Term Life Insurance

This is where the death benefit decreases each year. Often used to cover things like a mortgage, where the outstanding balance declines over time.

Return of Premium Term Life Insurance

As its name implies, if you outlive the term of the policy, you get back the premiums you paid. But this extra feature often comes with a higher price tag than standard term life insurance. This type of policy is typically more expensive.

Is Term Life Insurance Right for You?

Many people find this form of life insurance especially attractive when they have specific financial responsibilities or goals they want to protect for a defined period. For example, it’s a great way to help make sure a mortgage gets paid off, provide financial security for young children until they’re financially independent, or secure the finances of a business partnership during a critical phase. To buy term life insurance, it’s best to think about your current and future financial obligations.

Pros of Term Life Insurance

- Provides substantial coverage at an affordable cost. Studies have found that many overestimate life insurance premiums.

- Allows you to customize the term length and coverage amount to meet your needs and financial capabilities.

- The death benefit provides financial peace of mind for your loved ones should you die prematurely.

- Is a straightforward way to provide coverage and protect loved ones without complex investment features.

Cons of Term Life Insurance

- Does not provide lifetime coverage. You need to renew or consider other options once the term ends. And if you develop health issues while the term life insurance is active, getting new coverage after your term ends might be harder or more expensive.

- There’s no cash value element to build savings or borrow against. You simply pay for the death benefit protection. Once the term ends and you don’t renew, you won’t receive any money back unless you have the Return of Premium variety. However, according to Minnesota.gov those are rare and can be 2-4 times more expensive.

Before Getting a Term Life Insurance Quote

Just as you’d carefully choose an apartment, take time to consider a few important factors before getting your term life insurance quote:

How Much Coverage Do I Need?

Calculate your outstanding debts (like a mortgage, loans, credit cards), future financial needs (education costs for children, potential spousal support), and desired income replacement for your dependents. Then, you’ll have a good estimate of the coverage that’s right for you. This means “what is term life insurance mean” to your personal situation: protecting your unique obligations. If you’re married, you can purchase separate term life insurance policies. These are sometimes referred to as single premium policies.

How Long Do I Need Coverage?

Consider how long these financial responsibilities will likely last. Choose a term length that matches that period. Short term life insurance policies are typically available but come with a shorter term. Sometimes a limited term policy is all that is needed.

What Affects My Term Life Insurance Premium?

Several factors contribute to your premium cost. These include Your age, Health, and medical history, Lifestyle choices (like smoking habits), Chosen coverage amount, and term length.

The Cost of Term Life Insurance

Thankfully, you might be surprised to find that term life insurance is often more affordable than many believe. Factors such as your age, health, and chosen coverage amounts play a major role in how much you’ll pay in premiums. A medical exam may be required to get accurate pricing.

Check out average monthly life insurance costs to understand current rates. While these charts show typical pricing, always remember to get personalized quotes to get the best understanding of the cost for your individual situation.

Conclusion

Learning about how does term life insurance work gives you more control. Armed with this understanding, you are in a better position to decide if it’s the right choice for you. Term life is relatively inexpensive and provides protection for a set time period. If you die within that term, your loved ones get a payout to cover crucial costs and expenses, helping to ease the financial burden at a difficult time. As with any major decision, seeking the advice of a qualified financial advisor helps ensure you select the right kind of life insurance for your unique needs.

FAQs about what is term life insurance mean

Which is better, term life or whole life insurance?

There is no single best life insurance option as it depends on personal needs and preferences. Term life insurance, typically offering coverage for 10-30 years, often costs less initially, making it potentially suitable for temporary financial responsibilities such as covering a mortgage or providing for dependent children. On the other hand, whole life insurance, sometimes referred to as a permanent life policy offers permanent coverage but is often significantly more expensive. The application process for both is very similar.

How does term life insurance work?

Term life insurance provides coverage for a chosen duration (typically 10-30 years). You pay premiums regularly during the policy term. If you die within that timeframe, the designated beneficiaries receive the death benefit. Unlike permanent insurance options like universal life, term life policies typically do not have a cash value component. The simplest form of life insurance, it’s popular with those needing coverage for specific periods and who may prefer more budget-friendly premiums. These term life policies make up the majority of life insurance coverage active today. You’ll typically see people buy term as they need the life insurance coverage now, as opposed to later in life.

What happens to my term policy at the end of the term?

When a term life policy reaches its end, your coverage expires. You can choose to let the policy lapse or consider other options such as; renewing for another term, but often at a higher premium. Another option is to convert your existing policy to a permanent one like whole life insurance, sometimes referred to as a permanent life policy, but again at a potentially increased cost. Most term life insurance policies come with a conversion rider allowing you to do so.

Do you get your money back at the end of term life insurance?

Typically, no. Once the policy’s term concludes and no death benefit has been paid, you will not get a refund unless you have opted for a “return of premium” term life insurance policy, a relatively rare offering. This is unlike some universal life insurance policies where you can get some premiums paid back.

Can I renew my term life insurance after it expires?

Yes, most term life insurance policies include a renewable feature that allows you to extend your coverage for another term period after your original policy expires. However, there are several important considerations to keep in mind. When you renew, your premium will typically increase significantly because it will be based on your current age rather than your age when you first purchased the policy. Additionally, many policies have age limits on renewability, often capping renewals at age 70 or 75. The renewal process usually doesn’t require a new medical exam or health questionnaire, which is beneficial if your health has declined since you first purchased the policy. However, the guaranteed renewable feature means you can keep your coverage even if you’ve developed health conditions, though at the higher age-based rates. Instead of renewing, you might also consider converting your term policy to a permanent life insurance policy if your policy includes a conversion rider. This option typically must be exercised before the end of your term or before reaching a certain age specified in your policy. If you’re approaching the end of your term, it’s wise to contact your insurance provider well in advance to understand your renewal options, costs, and any deadlines for exercising conversion rights.

Can I cancel term life insurance early without penalty?

Yes, you can typically cancel a term life insurance policy at any time without facing penalties or surrender charges. Term life insurance functions similarly to other types of insurance coverage where you can simply stop paying premiums and allow the policy to lapse. Unlike whole life or other permanent insurance policies that build cash value, term life insurance has no cash value component, so there’s nothing to surrender or lose beyond the coverage itself. When you cancel, you won’t receive a refund of the premiums you’ve already paid unless your policy includes a return of premium rider. To cancel your policy, you should contact your insurance company directly and request cancellation in writing. Many insurers will ask you to complete a cancellation form. It’s important to ensure you have alternative coverage in place before canceling if you still need life insurance protection, as obtaining new coverage later may be more expensive due to increased age or changes in health. Some policies may have a grace period after a missed payment before they officially lapse, so if you’re considering cancellation, check your policy documents for specific details. If you’re canceling because of cost concerns, you might also explore options to reduce your coverage amount or convert to a different type of policy rather than canceling entirely.

Is term life insurance better than whole life insurance?

Neither term nor whole life insurance is universally “better” – the right choice depends entirely on your financial situation, goals, and budget. Term life insurance is typically six times more cost-effective than whole life for an equivalent death benefit, making it ideal if you need substantial coverage on a limited budget, have temporary financial obligations like a mortgage or dependent children, want straightforward protection without investment features, or are young and building financial stability. The main trade-off is that term coverage expires after the specified period, and you receive no benefits if you outlive the policy unless you have a return of premium rider. Whole life insurance, on the other hand, is better suited if you want lifelong coverage regardless of when you pass away, desire to build cash value you can borrow against or withdraw from, need a policy for estate planning purposes, want level premiums that never increase, or can comfortably afford higher premiums. However, whole life insurance costs significantly more – sometimes five to ten times more than term for the same death benefit amount. Many financial experts recommend term life insurance for most people because it provides maximum protection during the years when dependents rely on your income, and the money saved on lower premiums can be invested elsewhere for potentially better returns. That said, whole life can make sense for specific situations like estate planning, final expense coverage, or if you have a lifelong dependent with special needs.

What happens if I miss a premium payment on my term life insurance?

If you miss a premium payment on your term life insurance policy, you typically enter a grace period during which your coverage remains active. Most insurance companies provide a grace period of 30 to 31 days from the due date, allowing you time to make the payment without losing coverage. During this grace period, if you were to pass away, your beneficiaries would still receive the death benefit, though the missed premium would be deducted from the payout. If you don’t make the payment within the grace period, your policy will lapse, meaning your coverage ends and you’re no longer protected. Once a policy lapses, reinstatement is possible but not guaranteed. To reinstate a lapsed policy, you’ll typically need to submit a reinstatement application, pay all past-due premiums plus interest, and potentially undergo a new medical exam or provide evidence of insurability depending on how long the policy has been lapsed. The reinstatement period is usually limited to a few years after the lapse, often three to five years, after which reinstatement may no longer be an option and you’d need to apply for entirely new coverage. To avoid missing payments, consider setting up automatic payments from your bank account, which many insurers offer and may even provide a small discount for. If you’re experiencing financial hardship, contact your insurance company before missing a payment – some insurers offer temporary payment arrangements or options to reduce coverage temporarily rather than letting the policy lapse entirely.

Can I have both term and whole life insurance at the same time?

Yes, you can absolutely have both term and whole life insurance policies simultaneously, and many people use this strategy to maximize their coverage while managing costs effectively. This approach, sometimes called “layering” insurance coverage, allows you to combine the strengths of both policy types. For example, you might maintain a whole life policy with permanent coverage for final expenses, estate planning, or lifelong dependents, while also carrying a larger term policy to cover temporary needs like mortgage payments, income replacement while children are dependent, or business obligations during your working years. This strategy is particularly popular because whole life insurance provides a guaranteed death benefit and builds cash value but is expensive for large coverage amounts, while term life insurance offers high coverage amounts at affordable premiums but only for a limited time. By combining both, you ensure permanent base coverage through your whole life policy while addressing peak financial responsibility years with additional term coverage. Once your term policy expires – perhaps when your mortgage is paid off and children are financially independent – you’ll still maintain the whole life coverage. When considering this approach, make sure the total premium payments for both policies fit comfortably within your budget, the combined death benefits align with your actual financial needs, and you understand how each policy works. Many insurance companies will even offer package deals or discounts when you purchase both types of policies from them. Just remember to review your coverage needs regularly as your financial situation changes, and adjust your policies accordingly.