Your Guide to the Best Cyber Liability Coverage Options That Won’t Break the Bank

Last reviewed: June 2026

A small accounting firm in Ohio experienced a ransomware attack that encrypted all client files overnight. The recovery process cost $47,000 in forensic investigations, data restoration, and client notifications, expenses that nearly bankrupted the 12-person operation. Their general liability policy provided no coverage for cyber incidents, leaving them to absorb the entire financial impact.

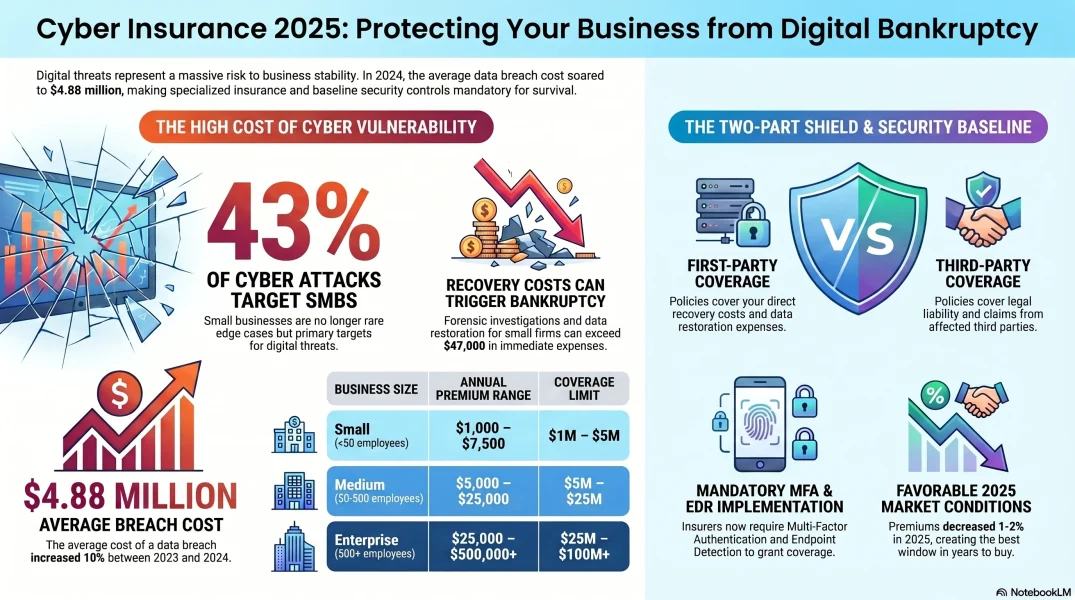

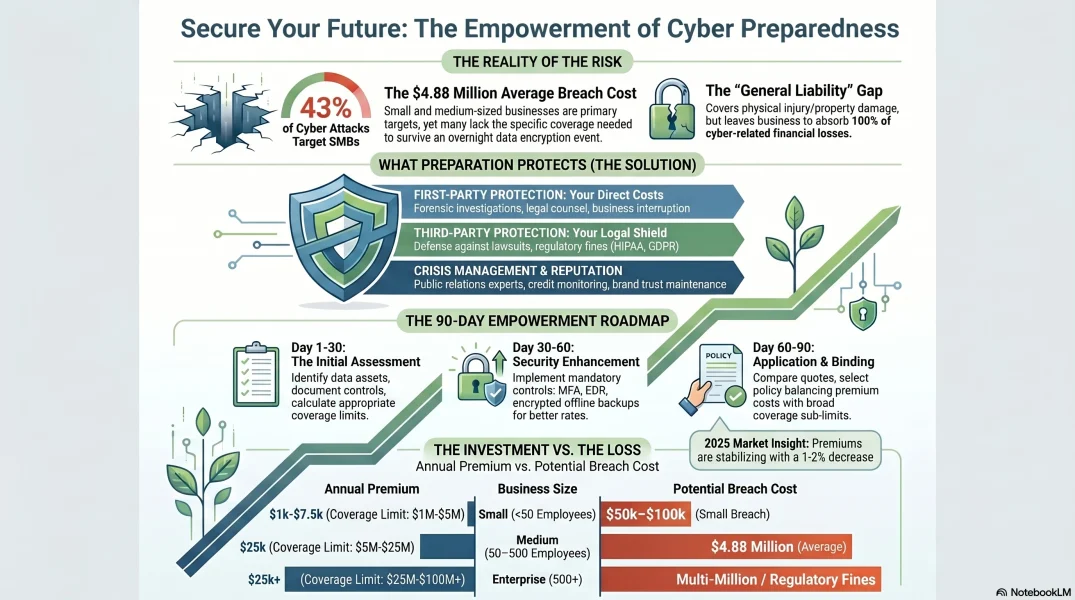

This isn’t a rare edge case. In 2024, 43% of cyber attacks targeted small and medium businesses, with the average data breach costing $4.88 million according to IBM Security’s annual report. The financial exposure extends beyond immediate recovery costs to include regulatory fines, legal fees, and long-term reputational damage.

Here’s what cyber liability coverage actually covers in 2025, who the leading providers are, what you’ll pay, and how to pick the right policy for your business size and risk profile.

Key Takeaways

| Option | Key Feature | Best For |

|---|---|---|

| What Cyber Liability Insurance Actually Covers | — | — |

| First-Party Coverage: Your Direct Costs | — | — |

| Third-Party Coverage: When Others Claim Against You | — | — |

| Leading Cyber Insurance Providers in 2025 | — | — |

| Chubb, Best for Established Enterprises | — | — |

| Coalition, Best for Proactive Risk Management | — | — |

| At-Bay, Best for Transparent Risk Insights | — | — |

| AIG, Best for International Operations | — | — |

| Travelers, Best for Small Businesses | — | — |

| Beazley, Best for Claims Experience | — | — |

- Cyber insurance premiums decreased 1-2% in 2025 after several years of increases, creating favorable market conditions

- Small business coverage typically ranges from $1,000-$7,500 annually for $1-5 million in protection

- Multi-factor authentication and endpoint detection systems are now baseline requirements for most insurers

- Coalition and At-Bay offer technology-driven underwriting with rapid quote generation

- Traditional carriers like Chubb (35.7% market share) and AIG (20.9% market share) maintain dominant positions

- Average data breach costs reached $4.88 million in 2024, representing a 10% increase from 2023

What Cyber Liability Insurance Actually Covers

Cyber liability insurance provides financial protection against losses resulting from data breaches, cyber attacks, and related digital security incidents. Unlike general liability insurance, which covers physical injuries and property damage, cyber policies specifically address digital risks that have become increasingly prevalent in modern business operations.

Coverage typically includes:

- Data breach response and notification costs

- Forensic investigations to determine breach scope and origin

- Legal defense costs for regulatory investigations and lawsuits

- Business interruption losses from cyber incidents

- Ransomware extortion payments and negotiation services

- Credit monitoring services for affected individuals

- Public relations and crisis management expenses

- Regulatory fines and penalties where legally insurable

Cyber insurance policies divide into first-party and third-party components, each addresses different aspects of your risk exposure.

First-Party Coverage: Your Direct Costs

First-party coverage addresses the costs the business incurs directly. Data breach response costs include forensic analysis to identify the breach source, legal counsel for regulatory compliance, notification expenses, and credit monitoring services. For businesses storing customer information, notification requirements escalate fast, notifying 10,000 affected individuals at $5-10 per notification creates immediate exposure of $50,000-$100,000.

Business interruption coverage compensates for income lost during system downtime. When ransomware disables operations, this coverage addresses lost revenue, continuing expenses during the interruption period, and extra costs to resume operations. For businesses dependent on digital systems, even 48-72 hours of downtime can result in significant financial impact.

Cyber extortion coverage provides resources for responding to ransomware attacks, negotiation services, ransom payments where legally permitted, and containment and investigation costs. Paying ransoms remains controversial, but policies provide this option along with expert guidance on response strategies.

Third-Party Coverage: When Others Claim Against You

Third-party coverage protects against liability claims from parties affected by your security failures. Privacy and network security liability covers legal defense costs, settlements, and judgments when data breaches lead to lawsuits from customers, partners, or other affected parties. Class action lawsuits following data breaches have become increasingly common, defense costs alone often exceed six figures before any settlement.

Regulatory defense and penalties coverage addresses government investigations and enforcement actions. With GDPR fines reaching up to 4% of global revenue, CCPA penalties of up to $7,500 per violation, and HIPAA fines ranging from $100-$50,000 per violation, regulatory exposure represents substantial risk for businesses handling personal information.

PCI penalties and assessments cover fines from payment card companies following breaches affecting cardholder data. These penalties can reach hundreds of thousands of dollars for businesses processing credit card transactions.

Leading Cyber Insurance Providers in 2025

The cyber insurance market in 2025 features both established carriers with decades of experience and technology-focused insurers leveraging data-driven underwriting. Here’s what each major provider actually does well.

Chubb, Best for Established Enterprises

Chubb maintains the largest market share at 35.7%, with $320.7 million in direct written premiums. Operating in 54 countries, Chubb provides comprehensive Cyber Enterprise Risk Management solutions designed for mid-market and large enterprises. Their coverage adapts to evolving business needs and includes access to a global network of breach response specialists.

Chubb’s underwriting process emphasizes thorough risk assessment, which typically results in more comprehensive coverage terms but requires more detailed security documentation. Minimum premiums generally start around $5,000 annually, this is a premium option for established businesses with mature security practices.

Coalition, Best for Proactive Risk Management

Coalition has achieved a $5 billion valuation through their “Active Insurance” model, combining traditional coverage with active security monitoring. Their Coalition Control platform provides continuous monitoring of policyholder security posture, identifying vulnerabilities and offering remediation guidance before breaches occur.

Their technology-first approach enables rapid quote generation, often providing bindable quotes within minutes rather than days. Pricing typically proves competitive for businesses with documented security controls, with many small and medium businesses receiving quotes in the $2,000-$5,000 annual range for $1 million in coverage.

At-Bay, Best for Transparent Risk Insights

At-Bay, valued at $1.35 billion, uses AI and extensive data analysis to generate instant risk assessments. Their platform scans business infrastructure during the application process, identifying security gaps and providing specific recommendations. This transparent approach shows applicants exactly which vulnerabilities affect their rates, which is genuinely useful beyond just the policy itself.

At-Bay works particularly well for technology companies and businesses with documented security programs, as their data-driven model recognizes and rewards strong security practices with favorable rates.

AIG, Best for International Operations

AIG commands 20.9% market share with $232.3 million in premiums, offering CyberEdge policies backed by decades of insurance expertise. Their 24/7 global breach response services and established claims-handling procedures provide reliability for businesses operating across multiple jurisdictions. AIG’s strength is financial stability and global reach, particularly suitable for businesses with international operations or complex coverage needs.

Travelers, Best for Small Businesses

Travelers has developed CyberFirst Essentials specifically for businesses with fewer than 50 employees. This streamlined product addresses the most common cyber risks facing small businesses while maintaining accessible pricing, many policies start around $1,000 annually. Their simplified application process and straightforward coverage terms make cyber insurance accessible to businesses that might find enterprise-focused policies overwhelming.

Beazley, Best for Claims Experience

Beazley has specialized in cyber risk for over two decades, earning 9.1% market share through their market-leading Breach Response product. They’ve handled thousands of breach incidents, that claims experience informs their underwriting and risk management guidance in ways newer entrants can’t match. Their breach response services include access to a vetted panel of forensics firms, legal counsel, and crisis management experts who can mobilize quickly following an incident.

Premium Costs and Coverage Limits

Cyber insurance premiums vary significantly based on business size, industry, security posture, and coverage limits. Here’s how the market typically breaks down by business category.

Small Business Costs (Under 50 Employees)

Annual premiums typically range from $1,000 to $7,500, with median costs around $2,000 for basic coverage. That’s roughly $167 per month for protection against cyber incidents. Coverage limits generally range from $1 million to $5 million, with deductibles between $1,000 and $25,000.

To put that in perspective: a modest data breach affecting 500 customer records can easily cost $50,000-$100,000 in response and notification expenses alone, far exceeding the annual premium cost.

Medium Business Investment (50-500 Employees)

Medium-sized businesses typically pay $5,000 to $25,000 annually, with coverage limits ranging from $5 million to $25 million. The wide premium range reflects variations in industry risk, data sensitivity, and security maturity. A 200-employee e-commerce company handling substantial customer data will face different pricing than a similar-sized manufacturing firm with limited data exposure.

Deductibles for medium businesses generally range from $25,000 to $100,000. Higher deductibles can reduce premiums by 10-25%, worth considering for businesses with adequate reserves.

Enterprise Protection (500+ Employees)

Large organizations typically invest $25,000 to $500,000 or more in comprehensive cyber protection, with coverage limits ranging from $25 million to $100 million or higher. While these premiums appear substantial, they represent a fraction of potential breach costs, the average $4.88 million breach cost would devastate most businesses without insurance protection.

Enterprise policies often include higher service levels, dedicated breach response coordinators, and access to top-tier forensics and legal resources. Deductibles typically start at $100,000 and can reach $1 million or more for very large organizations with significant risk tolerance.

Factors That Drive Your Premium

Understanding what moves the needle on pricing gives you leverage. Some of these factors you can control, and the savings are meaningful.

Industry and Data Sensitivity

Healthcare providers, financial institutions, and technology companies face higher premiums due to the sensitive nature of their data and strict regulatory requirements. HIPAA-regulated entities typically pay 30-50% more than comparable businesses in less-regulated industries. The volume and type of personal information you store, credit card data, Social Security numbers, health records, financial accounts, significantly impacts pricing.

Security Controls and Practices

Security posture is the most controllable factor affecting your premium. Multi-factor authentication can reduce premiums by 5-10%. Endpoint detection and response systems may lower costs by 10-15%. Regular vulnerability assessments, employee security training, and documented incident response plans all contribute to favorable underwriting decisions.

Businesses demonstrating mature security practices through certifications like SOC 2, ISO 27001, or NIST Cybersecurity Framework alignment often receive preferential rates. These certifications provide third-party validation that reduces perceived risk from the insurer’s perspective.

Revenue and Geographic Scope

Higher revenue correlates with higher premiums, reflecting increased business interruption exposure. Multi-state or international operations increase complexity and cost, as businesses must comply with varying data protection regulations across jurisdictions.

Companies operating in or selling to the European Union face GDPR compliance requirements that can increase premiums by 15-25%. Similarly, businesses subject to CCPA, CPRA, or other state-level privacy laws face additional compliance costs reflected in insurance pricing.

Security Requirements to Get Coverage

Cyber insurance carriers have established baseline security requirements that businesses must meet to obtain coverage. These requirements reflect lessons learned from thousands of claims, and they represent genuine best practices, not just paperwork.

Mandatory Controls

Multi-factor authentication for all administrative and privileged accounts has become a universal requirement. This single control prevents the vast majority of credential-based attacks, insurers know it, and they require it.

Endpoint detection and response (EDR) software across all devices represents another near-universal requirement. Traditional antivirus no longer provides sufficient protection against modern threats, which is why insurers now mandate more sophisticated endpoint security.

Regular software updates and patch management must be documented and demonstrable. Insurers increasingly verify that businesses maintain current software versions and apply security patches within reasonable timeframes.

Encrypted backups stored offline or in immutable storage have become mandatory. Ransomware attacks specifically target backup systems, protected backups are essential for recovery, and insurers know it.

Written incident response plans outlining breach detection, escalation, and response procedures demonstrate organizational preparedness. Plans don’t need to be complex, but they must address key response components and assign specific responsibilities.

Controls That Can Reduce Your Premium

Security awareness training for all employees, conducted at least annually, can reduce premiums by 5-10%. Human error remains a primary cause of security incidents, this is one of the most cost-effective risk reduction investments available.

Annual penetration testing or vulnerability assessments by qualified third parties demonstrate commitment to proactive security. These provide valuable insights while supporting favorable insurance terms.

Privileged access management systems controlling and monitoring administrative account usage can reduce premiums by 5-8%. Network segmentation limiting lateral movement following a breach represents an advanced control that sophisticated insurers recognize with premium reductions.

Policy Exclusions: Know Your Gaps Before You Need Coverage

Standard cyber policies typically exclude several categories of incidents. Understanding these before you buy prevents unpleasant surprises during a claim.

War and State-Sponsored Attacks

Most policies exclude losses from war, hostile military actions, or attacks by nation-state actors. This exclusion has generated considerable debate following high-profile attacks attributed to state-sponsored groups. Some policies now offer limited coverage for state-sponsored attacks through specific endorsements, ask about this if it’s a relevant risk for your business.

Prior Known Circumstances

Policies exclude claims arising from incidents or circumstances known to the insured before policy inception. Address known vulnerabilities before applying for coverage, and disclose security incidents honestly during the application process.

Failure to Maintain Security Standards

Coverage may be denied if you fail to maintain required security controls. Disabling MFA, discontinuing endpoint protection, or abandoning other mandated controls can void coverage for resulting incidents. Cyber insurance requires ongoing security commitment, not just controls in place at policy purchase.

Infrastructure Improvement Costs

Policies cover restoration to pre-incident status but exclude costs for system upgrades or improvements. If outdated systems contributed to a breach, insurance covers restoring those systems, not upgrading to more secure alternatives. You cannot use insurance proceeds to fund technology modernization.

How to Get Covered: A Practical Timeline

Getting cyber insurance requires systematic preparation. Plan for 60-90 days from start to active coverage, longer if you have security gaps to address first.

Initial Assessment Phase (30 Days)

Conduct a comprehensive risk assessment identifying data assets, processing activities, and potential exposure. Document existing security controls and practices. Calculate appropriate coverage limits based on potential business interruption costs, data breach notification expenses, and regulatory exposure.

Obtain preliminary quotes from multiple carriers to understand available options and pricing. Working with specialized cyber insurance brokers provides access to more carriers and expertise in comparing policy terms beyond just premium costs.

Security Enhancement Phase (30-60 Days)

Implement mandatory security controls required by insurers. Deploy MFA across administrative accounts, implement or upgrade endpoint detection systems, establish regular backup procedures with offline storage, and develop written incident response procedures.

Document all security improvements, insurers increasingly verify security claims through technical assessments, making documentation essential for underwriting approval.

Application and Binding Phase (30 Days)

Submit formal applications with complete security documentation. Compare quotes not just on premium cost but on coverage breadth, sub-limits, deductibles, and policy terms. Pay particular attention to exclusions, sub-limits for specific coverages, and requirements for maintaining coverage throughout the policy period.

Market Conditions and Outlook

The cyber insurance market has stabilized significantly from the volatile conditions of 2020-2022. Following several years of dramatic premium increases and capacity restrictions, rates decreased 1-2% in 2025 for the first time since 2019, creating favorable conditions for businesses seeking coverage now.

More stringent security requirements have reduced claim frequency and severity. Increased competition among carriers has improved availability. Enhanced underwriting sophistication has enabled more accurate risk pricing. These improvements stack in your favor if you’re buying now.

The global cyber insurance market reached $15.3 billion in 2024 and is projected to grow to $16.3 billion in 2025. By 2030, market analysts project the market will exceed $30 billion as cyber insurance becomes standard business practice, which means tighter requirements and potentially higher rates for businesses that wait.

Looking forward, AI will increasingly influence both cyber attacks and defensive capabilities, requiring coverage evolution. Supply chain cyber risks will demand new products addressing third-party exposures. Expanding privacy regulations globally will increase compliance costs and related coverage needs.

Start Now, Current Conditions Won’t Last

Cyber liability insurance has moved from a specialty product to essential business protection. The 2025 market offers businesses unprecedented access to comprehensive coverage at increasingly competitive rates, but that window won’t stay open indefinitely.

For most small businesses, the right starting point is implementing the mandatory security controls, MFA, endpoint detection, offline backups, incident response documentation, then getting quotes from 3-4 carriers, including at least one technology-driven provider like Coalition or At-Bay. The quote process will surface gaps in your security posture and help you understand what you’re actually buying.

The fundamental question isn’t whether to get cyber insurance, it’s how quickly you can implement the security controls required for coverage. With average breach costs approaching $5 million and recovery timeframes extending months or years, operating without coverage is a bet that most businesses can’t afford to lose.

Frequently Asked Questions

How do I determine appropriate coverage limits for my business?

Calculate coverage needs by assessing potential first-party costs (business interruption, breach notification, forensics) and third-party liability exposure (lawsuits, regulatory fines). Consider your revenue, amount, and sensitivity of data held, regulatory requirements, and contractual obligations. Most small businesses need $1-5 million in coverage, medium businesses $5-25 million, and large enterprises $25-100 million or more. Consult with a specialized broker to model specific scenarios relevant to your business operations and risk profile.

What distinguishes cyber insurance from general liability coverage?

General liability covers bodily injury and property damage from physical incidents. Cyber insurance specifically addresses digital risks, data breaches, cyber attacks, and business interruption from technology failures. General liability policies typically exclude cyber incidents explicitly, creating a coverage gap that cyber insurance fills. Businesses need both: general liability for physical risks and cyber insurance for digital exposures.

Can businesses obtain coverage without implementing MFA or EDR?

In 2025, virtually all cyber insurers require multi-factor authentication on administrative accounts as a baseline control. Endpoint detection and response has become similarly mandatory for most carriers. Some insurers may provide limited coverage without these controls at substantially higher premiums, but such policies typically include restrictive terms and lower limits. The practical approach: implement required controls before applying, since these security measures provide protection value well beyond insurance requirements.

Does cyber insurance cover ransomware payments?

Most cyber insurance policies include cyber extortion coverage that can pay ransom demands, subject to policy limits and conditions. Coverage typically includes negotiation services, payment facilitation, and forensic investigation costs. However, policies exclude payments to sanctioned entities or in violation of applicable laws. Many experts recommend against paying ransoms due to uncertain outcomes and encouragement of criminal activity, but policies provide this option for situations where payment represents the least harmful alternative. Importantly, policies also cover the substantial costs of containment, investigation, and recovery that often exceed ransom amounts.

How long does the coverage application process typically take?

Timeline varies by business size and complexity. Small businesses with documented security controls may obtain coverage within 1-2 weeks using streamlined applications from carriers like Coalition or At-Bay. Medium and large businesses should anticipate 4-8 weeks for comprehensive underwriting, security assessments, and policy negotiation. Businesses without required security controls should add 30-60 days for implementation before applying. Start the process 3-6 months before needed coverage, that timeline enables security improvements and a thorough market comparison without deadline pressure.

What happens if security controls fail or are disabled after obtaining coverage?

Cyber insurance policies require maintaining security controls throughout the policy period. Disabling mandatory controls like MFA or endpoint detection may void coverage for resulting incidents. If controls must be temporarily disabled for legitimate business reasons, notify your insurer immediately and implement compensating controls. Document all security control changes and maintain evidence of compliance to support potential claims.

{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”How do I determine appropriate coverage limits for my business?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:”Calculate coverage needs by assessing potential first-party costs (business interruption, breach notification, forensics) and third-party liability exposure (lawsuits, regulatory fines). Most small businesses need $1-5 million in coverage, medium businesses $5-25 million, and large enterprises $25-100 million or more. Consult with a specialized broker to model scenarios relevant to your operations and risk profile.”}},{“@type”:”Question”,”name”:”What distinguishes cyber insurance from general liability coverage?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:”General liability covers bodily injury and property damage from physical incidents. Cyber insurance specifically addresses digital risks, data breaches, cyber attacks, and business interruption from technology failures. General liability policies typically exclude cyber incidents explicitly, creating a coverage gap that cyber insurance fills, so businesses need both.”}},{“@type”:”Question”,”name”:”Can businesses obtain coverage without implementing MFA or EDR?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:”In 2025, virtually all cyber insurers require multi-factor authentication on administrative accounts as a baseline control, and endpoint detection and response has become similarly mandatory for most carriers. Some insurers may provide limited coverage without these controls at substantially higher premiums, but the practical approach is to implement required controls before applying.”}},{“@type”:”Question”,”name”:”Does cyber insurance cover ransomware payments?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:”Most cyber insurance policies include cyber extortion coverage that can pay ransom demands, subject to policy limits and conditions, including negotiation services, payment facilitation, and forensic investigation costs. However, policies exclude payments to sanctioned entities or in violation of applicable laws. Policies also cover the substantial costs of containment, investigation, and recovery that often exceed ransom amounts.”}},{“@type”:”Question”,”name”:”How long does the coverage application process typically take?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:”Timeline varies by business size and complexity. Small businesses with documented security controls may obtain coverage within 1-2 weeks using streamlined applications from carriers like Coalition or At-Bay. Medium and large businesses should anticipate 4-8 weeks. Businesses without required controls should add 30-60 days for implementation, so start the process 3-6 months before needed coverage.”}},{“@type”:”Question”,”name”:”What happens if security controls fail or are disabled after obtaining coverage?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:”Cyber insurance policies require maintaining security controls throughout the policy period. Disabling mandatory controls like MFA or endpoint detection may void coverage for resulting incidents. If controls must be temporarily disabled for legitimate business reasons, notify your insurer immediately and implement compensating controls, documenting all changes to support potential claims.”}}]}